Think of insurance for your window cleaning business as your ultimate safety net. It’s what stands between a simple on-the-job accident and a financial catastrophe that could shut your doors for good. When you're dealing with potential property damage, client injuries, or harm to your crew, insurance turns a business-ending disaster into a manageable problem.

Why Window Cleaning Insurance Is Non-Negotiable

Let's cut right to it. Running a window cleaning business without insurance is like working on a high-rise without a safety harness. You might get away with it for a while, but you're one slip away from total disaster. Relying on luck isn't a business plan—it's a gamble you can't afford to lose.

The risks are real and they happen every day. A dropped squeegee can shatter a priceless antique window. A ladder leg can sink into soft ground and knock over a client's expensive statue. A simple slip on a wet floor can lead to a lawsuit that drags on for months.

Understanding the Financial Stakes

Without the right coverage, you're on the hook for every penny of those costs. A single lawsuit or major property damage claim could easily wipe out your business and even put your personal assets at risk. This is why smart owners see insurance not as a burdensome expense, but as a core part of their business foundation. It protects your livelihood and signals to clients that you're a true professional.

This financial shield is more important than ever. The U.S. window cleaning market is set to grow from $2.9 billion in 2024 to $3.2 billion by 2029, which means more competition and higher client expectations for professionalism and safety.

Having the right insurance policies is what separates a minor, frustrating setback from a complete business shutdown. It gives you the peace of mind and financial stability to handle the unexpected without having to drain your own bank account.

Good insurance is also a cornerstone of effective business continuity planning, ensuring that one bad day doesn't permanently disrupt your operations. Foundational policies like General Liability and Workers' Comp are your first line of defense, covering critical scenarios like:

- Third-Party Property Damage: For when you accidentally crack a window or scratch expensive flooring.

- Bodily Injury to a Third Party: Covers you if a client, visitor, or pedestrian trips over your hose and gets hurt.

- Employee Injuries: Pays for medical bills and lost wages if one of your team members is injured on the job.

Decoding Your Core Insurance Policies

Let’s be honest, insurance can feel like a foreign language. But once you get the hang of it, you'll see it for what it is: a safety net that protects everything you're working so hard to build. Think of your policies as a specialized toolkit—each one designed to handle a specific risk you’ll face out in the field.

We're going to break down the must-have insurance for any serious window cleaning business, without the confusing jargon.

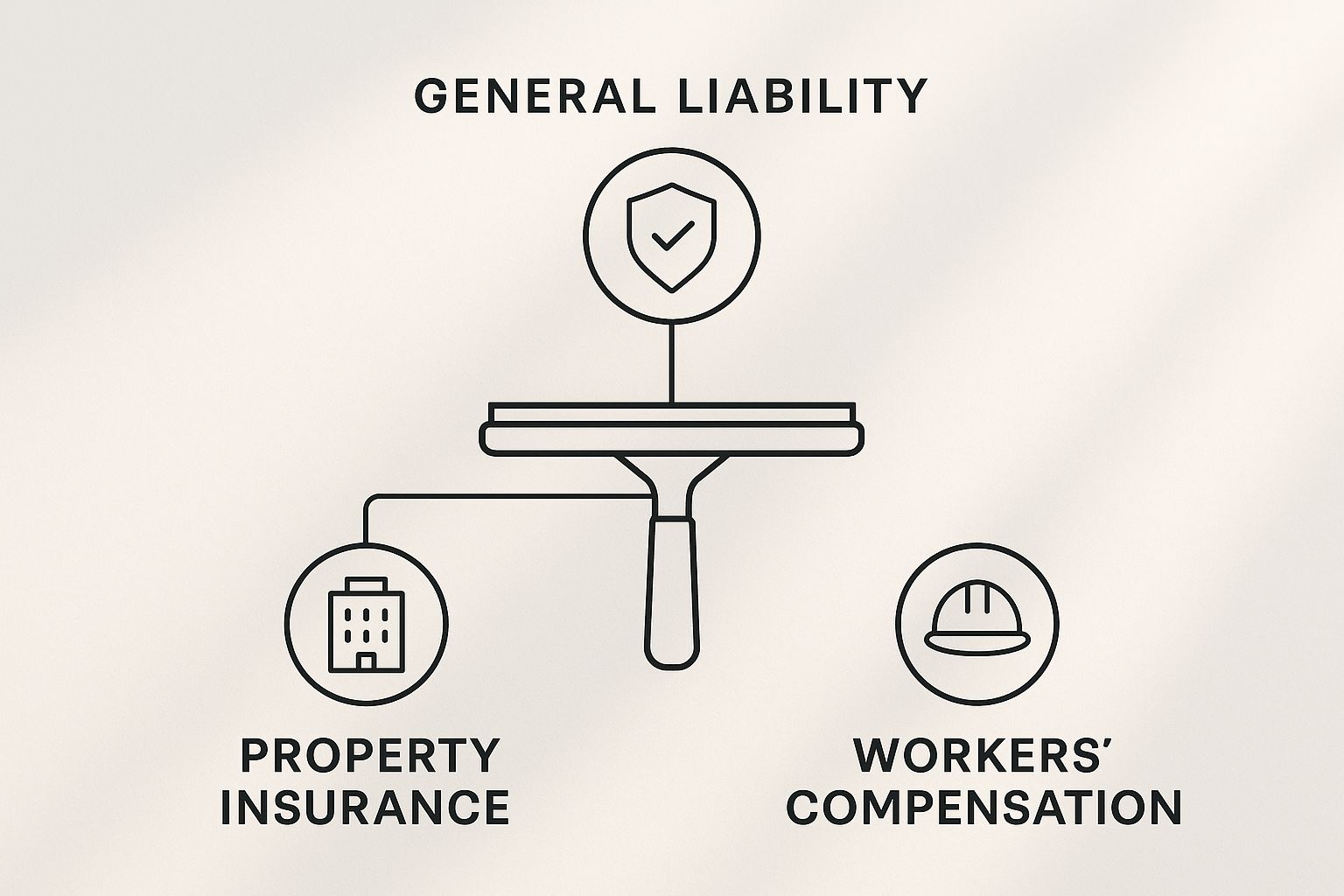

This image nails the three pillars of protection: General Liability, Workers' Comp, and Property Insurance. Together, they create a shield around your business, protecting you from client accidents, employee injuries, and equipment damage.

General Liability: The Foundation Of Your Protection

If you only get one policy, make it this one. General Liability Insurance is the absolute bedrock of your coverage. It’s your shield against claims from third parties—basically, anyone who isn't on your payroll—for injuries or property damage your work might cause. This is your primary defense against the everyday "oops" moments that can happen on any job.

Here’s a classic example: one of your crew is up on a ladder, and a squeegee slips from their grip. It tumbles down and lands squarely on the client's brand-new luxury car, leaving a nasty dent and a long scratch. Without insurance, that repair bill is coming straight out of your pocket. We're talking thousands of dollars for a simple, honest mistake.

With a good general liability policy, however, you'd file a claim, and the insurance would cover the repair costs. It’s a financial firewall. Most policies for cleaners have a $1 million per-occurrence limit, which gives you serious peace of mind.

Workers’ Compensation: Protecting Your Most Valuable Asset

The second you hire your first employee—even a part-timer—Workers’ Compensation Insurance becomes a necessity. In nearly every state, it’s not just a good idea; it’s the law. This policy is essentially a pact that protects both you and your team.

If an employee gets hurt on the job, workers' comp steps in to cover their:

- Medical Bills: From the initial emergency room visit to ongoing physical therapy.

- Lost Wages: A portion of their income is replaced while they recover and can't work.

- Disability Benefits: Provides financial support if the injury causes a temporary or permanent disability.

In exchange for these guaranteed benefits, the employee generally can't sue you for the injury. This protects your business from a lawsuit that could sink it, all while ensuring your crew gets the medical care they need to get back on their feet.

Commercial Auto and Inland Marine: Covering Your Gear On The Go

Your work vehicle and all the gear inside are the lifeblood of your business. A standard personal auto policy won't touch a claim if an accident happens while you're driving for work, which is why Commercial Auto Insurance is non-negotiable. It covers your work truck or van for both liability and physical damage.

But what about the expensive equipment in the back? Your water-fed pole system, pressure washer, and specialized ladders aren't covered by commercial auto or a standard property policy once they leave your shop. This is where a policy called Inland Marine Insurance saves the day.

Think of Inland Marine coverage as insurance for your tools in transit. It protects your valuable equipment whether it’s in your truck, on a job site, or temporarily stored somewhere else.

To make things simpler, here’s a quick rundown of the essential coverages.

Your Essential Window Cleaning Insurance Toolkit

This table sums up the core policies, what they do, and when you'd actually need them.

| Coverage Type | What It Protects Against | Real-World Scenario |

|---|---|---|

| General Liability | Bodily injury or property damage to third parties (e.g., clients, pedestrians). | Your ladder accidentally falls and breaks a client’s expensive custom window. |

| Workers' Comp | On-the-job injuries or illnesses sustained by your employees. | An employee slips on a wet surface and fractures their wrist, requiring surgery and time off. |

| Commercial Auto | Accidents involving your work vehicle, covering liability and vehicle damage. | You rear-end another car while driving between job sites in your company van. |

| Inland Marine | Theft, loss, or damage to your tools and equipment while in transit or at a job site. | Your truck is broken into overnight and all your high-end squeegees and poles are stolen. |

For many window cleaners, especially those just starting out or running a smaller operation, a Business Owners Policy (BOP) can be a fantastic, budget-friendly option. A BOP bundles general liability and property insurance (which can include your gear) into a single, more affordable package.

Getting your insurance sorted is a fundamental part of learning https://sparkletechwindowwashing.com/how-to-start-window-cleaning-business/ and building a business that’s designed to last.

Understanding What Drives Your Insurance Costs

So, you're looking for insurance for your window cleaning business. The big question on your mind is probably, "How much is this going to set me back?" The truth is, there's no single price tag. Your premium is calculated based on your company's specific risk profile.

Think of it just like car insurance. A new driver with a flashy sports car is going to pay a lot more than a seasoned driver with a reliable sedan because the risk is worlds apart. It's the same principle here. Insurance providers look at the unique risks tied to your window cleaning operation to figure out your final premium.

Your Business Operations and Size

The biggest factor influencing your cost is the kind of work you do every day. A one-person operation focusing on single-story homes is a much lower risk than a ten-person crew scaling high-rise commercial buildings. The higher you climb, the greater the chance of a serious accident, and you can bet your premiums will reflect that.

But it doesn't stop there. Insurers will also dig into other details:

- Number of Employees: More people on your team means more opportunities for workers' comp claims. Your total payroll is a huge part of this calculation.

- Annual Revenue: Bringing in more money usually means you're taking on more jobs. This increased activity naturally increases your exposure to potential liability, which can bump up your premium.

- Claims History: A spotless record is your best friend. If you have no past claims, it tells insurers you run a tight, safe ship, which often leads to better rates.

To put some numbers on it, a small window cleaning business with a couple of employees and around $300,000 in annual revenue could expect to pay somewhere between $62 and $234 per month. These plans typically include a $1 million per occurrence liability limit, which is a solid safety net.

Your insurance premium is a direct reflection of your business's risk. The safer your operations, the more favorable your rates will be. Proving you have a strong safety culture is one of the best ways to manage your long-term costs.

Your Policy Choices and Coverage Limits

Just as important as what you do is what you choose for your policy. You have direct control over two key levers that will raise or lower your final price: coverage limits and deductibles.

A coverage limit is simply the maximum amount your insurance company will pay out for a single covered claim. A $1 million general liability limit is pretty standard for the industry. However, if you land a large commercial contract, they might require a $2 million limit or even ask you to get an umbrella policy for extra protection. Higher limits mean more peace of mind, but they also come with a higher premium. Knowing the average cost of window washing can help you fit these essential business expenses into your budget.

Then there's your deductible. This is the amount you have to pay out of your own pocket before your insurance coverage starts paying. If you choose a higher deductible—say, $2,500 instead of $500—you'll see your monthly premium go down. The catch is making sure you can comfortably afford that deductible on a moment's notice if something goes wrong. It's all about finding that sweet spot between a manageable premium and a deductible you can actually pay.

Meeting Client and State Requirements

Having the right insurance for your window cleaning business isn't just a smart way to protect yourself—it’s often the price of admission. Think of your insurance policies as a key that unlocks access to bigger contracts and serious clients who expect you to operate like a true professional.

Before you even worry about what clients want, you have to get square with the law. The moment you hire your first employee, most states have a non-negotiable rule: you must carry Workers' Compensation insurance. It doesn’t matter if they’re full-time or part-time. Skipping this can lead to massive fines or even get your business shut down.

Winning Client Trust with a Certificate of Insurance

Once you've handled your legal duties, you’ll find that your clients have their own set of rules. Commercial property managers, general contractors, and high-end homeowners won't just take your word for it that you're covered. They'll ask for proof—a Certificate of Insurance (COI)—before you can set foot on their property.

A COI is just a one-page snapshot of your insurance, showing what policies you have and your coverage limits. It's like an ID card for your business's insurance. It's the quickest way to show a potential client you’re serious and that you respect their property. If you can't produce a COI that meets their standards, your bid is probably going straight into the trash.

Your Certificate of Insurance is more than just a piece of paper. It's a powerful marketing tool that instantly communicates reliability, trustworthiness, and financial stability to potential clients.

This simple document is absolutely essential for landing better-paying jobs. Many commercial clients, for example, will set a minimum general liability limit of $1 million per occurrence and a $2 million aggregate. Being able to hand that over without hesitation is what separates you from the amateurs.

The Power of Being Bonded and Insured

You’ve probably seen "Licensed, Bonded, and Insured" on the side of a work truck. There's a good reason for that. While insurance is there to cover accidents, a surety bond—specifically, a janitorial or business service bond—is there to protect your client from something else: theft.

It breaks down like this:

- Insurance: Pays for accidents, like a broken window or an injury.

- Bonding: Reimburses your client if one of your employees is caught stealing.

Having both tells clients you’ve got them covered from every angle, and that builds incredible trust. In fact, a recent survey found that 30% of insured cleaning businesses said their coverage directly helped them land more contracts.

When you meet these requirements, you're not just buying a policy. You're investing in a tool that lets you confidently bid on the bigger, more profitable jobs you really want.

Finding the Right Insurance Partner

Picking an insurance provider isn't like ordering squeegees off Amazon. This is a real partnership, and it needs to be built on trust. You need someone who gets that the risks of washing a ranch-style home are a world away from rappelling down a high-rise.

A generic policy just won't do the job. The right partner speaks your language. They know what a water-fed pole is, they understand the unique liabilities of high-rise work, and they won't look at you funny when you ask about coverage for your gear while it’s in the truck. You're looking for a specialist, not a jack-of-all-trades.

How to Vet Potential Insurance Providers

Before you sign on the dotted line, you’ve got to do your homework. A cheap premium is worthless if the company ghosts you when you actually need to file a claim. Your mission is to find an insurer who hits the sweet spot between reliability, industry knowledge, and a fair price.

The best way to start is with a simple checklist. It'll keep you organized and help you compare apples to apples.

Here’s what you need to dig into:

- Industry Specialization: Be direct. Ask them how many other window cleaning businesses they insure. Do they have policies built specifically for trade professionals like you?

- Financial Stability: Check their rating with an independent agency like A.M. Best. You want to see a high rating (A- or better), which means they have the cash to pay claims without breaking a sweat.

- Claims Process: What’s it like to actually file a claim? Read online reviews. Ask them what their typical turnaround time is. A clunky claims process is the last thing you want to deal with when something goes wrong.

- Customer Service: Give their support line a call. Are they easy to get a hold of? Do they sound like they know what they’re talking about? This is a great preview of the service you'll get as a customer.

Comparing Quotes the Smart Way

Once you’ve got a shortlist of providers who pass the sniff test, it's time to get some quotes. But don't just jump at the lowest number. A cheap quote could be hiding a dangerously high deductible or leaving out coverage you absolutely need.

When you compare insurance quotes, you're not just shopping for a price—you're shopping for a promise. Make sure that promise actually covers what your business needs by looking at the coverage limits, exclusions, and deductibles side-by-side.

Look for providers known for that balance of cost and great service. Insurers like The Hartford, Thimble, and Nationwide often come up in conversation because they have strong offerings for businesses like ours. They're a great place to start your search and give you a solid benchmark for both cost and coverage. You can learn more about how top insurers stack up on moneygeek.com to get a better sense of the landscape.

Remember, focusing on value over just the sticker price will land you a partner who’s truly got your back, helping you protect and grow your window cleaning business for years to come.

Common Questions About Window Cleaning Insurance

Trying to wrap your head around insurance for your window cleaning business can feel like a job in itself. You're focused on getting streak-free results for your customers, not translating dense policy documents. To make things easier, I've put together some straight-to-the-point answers for the questions I hear most often from other window cleaners.

This isn't about legal jargon or complicated theories. It’s a practical guide to help you make smart, confident choices to protect the business you're working so hard to grow. Let's get right into it.

Do I Really Need Insurance as a Solo Operator?

Yes, absolutely. It comes down to two big things: protection and professionalism. When you're a solo operator, you are the business. That means if an accident happens, your personal assets—your house, your truck, your savings—are on the line to cover damages or legal bills.

Think about it. You're working two stories up and a squeegee slips, landing on your client's brand-new luxury car. That's a gut-wrenching moment. A general liability policy is what stands between that expensive mistake and your personal bank account. Beyond that, being insured signals that you're a true professional, which helps you land better jobs. Most clients, especially the high-value ones, won't even consider hiring someone who isn't insured.

A single accident could jeopardize everything you’ve worked for. Insurance turns a potential financial disaster into a predictable business cost, protecting your company and your personal life from day one.

What Is the Difference Between Being Insured and Bonded?

This is a huge point of confusion for a lot of people, but the difference is simple and important. Insurance protects your business from accidents. A bond protects your client from theft or dishonesty.

- Insurance: This is for accidental risks. If you accidentally crack a window or a homeowner trips over your hose, your general liability insurance is there to pay for the damage or medical costs. It’s for the "oops" moments.

- Bonding: This is about your integrity. If an employee is convicted of stealing jewelry from a client’s home, a janitorial bond (which is a type of surety bond) pays the client back for their loss.

Here's the easiest way to remember it: insurance is for what you break, and bonding is for what you take. Having both is the gold standard that serious commercial and residential clients expect.

How Can I Lower My Insurance Premiums?

Good news—you have more control over your insurance costs than you might think, and it doesn't mean cutting corners on coverage. The single best way to lower your premiums over the long haul is to build a rock-solid safety record. When insurers see you have no claims, they see you as a low-risk business.

Here are a few practical steps you can take to get better rates:

- Create a Real Safety Program: Don't just talk about safety—document it. Write down your procedures, hold quick trainings, and check your equipment regularly. When you can show an insurer you’re serious about preventing accidents, they're more likely to give you a better price.

- Bundle Your Policies: Ask your insurance agent about a Business Owner's Policy (BOP), which combines general liability and property insurance. You can often get a discount for bundling policies, just like with home and auto insurance.

- Choose a Higher Deductible: The deductible is what you pay out of pocket before your insurance starts paying. If you raise your deductible from, say, $500 to $2,500, your monthly premium will go down. Just make sure you have enough cash set aside to comfortably cover that higher amount if you ever need to make a claim.

For more answers to other operational questions, check out our guide covering common questions about window cleaning.

At Sparkle Tech Window Washing, we know that being properly insured is fundamental to being a professional service. We are fully insured and bonded because we want our clients in Phoenix and across Arizona to have total peace of mind every time we're on their property. To see what a difference a protected, professional team makes, visit us at https://sparkletechwindowwashing.com.